Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

As we head into the New Year and continue analyzing how to overcome affordability challenges in today’s market, I wanted to cover another important topic. In my last newsletter, we discussed house hacking strategies for first time buyers and the importance of remaining realistic about your budget and what to focus on in order to make a purchase to start building wealth and stop renting.

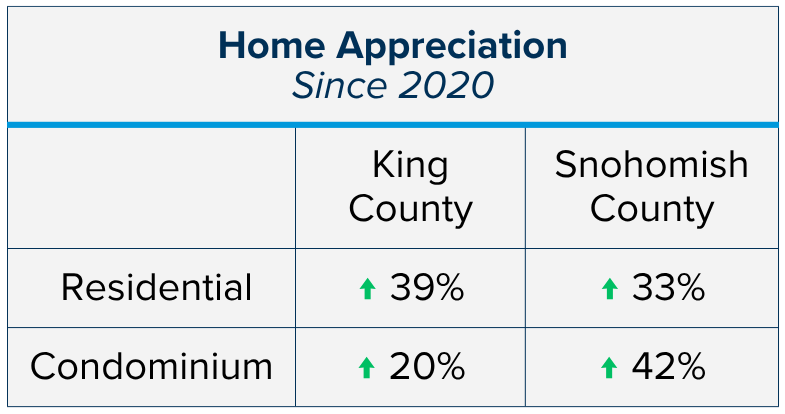

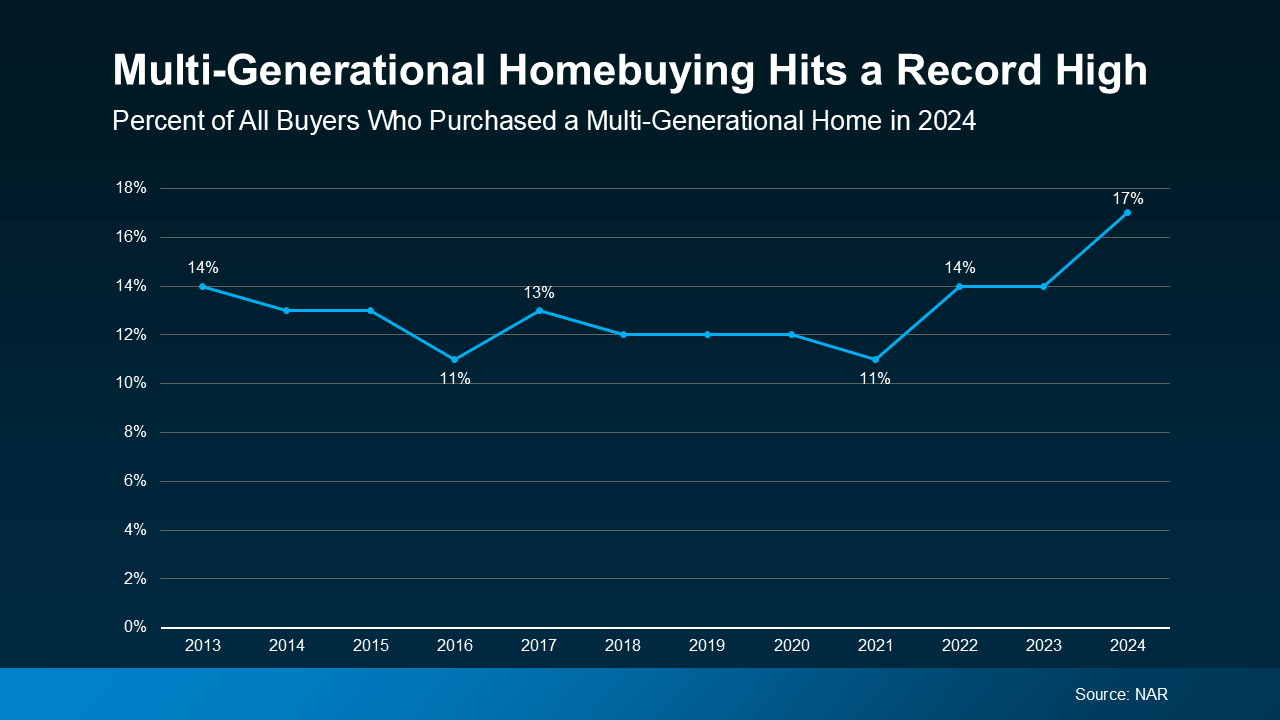

Another group that I’ve seen face affordability challenges are older adults whose homes no longer support their lifestyle or their current or future care needs. House hacking tips for multigenerational households is a growing trend that is worth shedding some light on. With prices remaining stable year-over-year and interest rates slowly receding, one needs to understand that values are maintaining, and creativity and strategy matter. One of the biggest conversations I’m having with clients lately—across all ages—is this: How do we stay housed, stay connected, continue to build wealth, and stay financially stable as costs keep rising?

For first-time buyers and move-up buyers, affordability can feel out of reach. For retirees on fixed incomes, housing and future care costs feel uncertain and incredibly expensive. For families, the increasing price of assisted living can be overwhelming—financially and emotionally. This isn’t just about real estate, it’s about how we take care of one another while staying financially resilient.

We were recently able to assist a first-time buyer family who was able to qualify for a mortgage with gift funds for the down payment from their parents. The monthly payments were intimidating to handle on their own with other monthly costs to consider, like childcare. Their parents were living in a retirement community that was costing a lot every month. They pooled their resources with the gift funds, the parents shifted out of the expensive retirement community, they shopped for a home with two separate levels plus room for a second kitchen, and a level entry to the daylight basement. The parents agreed to contribute to the monthly payments, which saved them substantially on their monthly overhead versus the retirement community. Now, both families are building wealth, no one is renting, and they are living comfortably and lovingly together.

There are solutions that help all ages obtain homeownership. One of the most powerful (and often overlooked) is multi-generational house hacking. This isn’t about cramming people together. It’s about thoughtful housing design and smart financing that allows families to live independently together, reduce monthly costs, and build long-term security. Here’s what that looks like in practice.

Independence First, Together by Design

The most successful multi-generational homes are designed with privacy and dignity in mind. This can include:

- A home with an ADU (accessory dwelling unit)

- A duplex or triplex where one unit is owner-occupied

- A daylight basement or in-law suite with a separate entrance

- Side-by-side living arrangements

- A second kitchen, or kitchenette, or space to build one is a bonus

When each generation has their own space, kitchens, and entrances when possible, relationships stay healthier—and living together becomes sustainable.

Housing as Cost Sharing, Not Sacrifice

In these setups, pooling funds and co-buying, having one family member rent space or contribute to the monthly mortgage, are best viewed as shared housing costs, not profit. Even modest monthly contributions can help cover:

- Mortgage payments

- Property taxes and insurance

- Utilities and maintenance

For retirees on fixed incomes, this can dramatically reduce financial pressure. For younger buyers, it can be the difference between qualifying for a home or staying on the sidelines.

Buy a Home That Can Grow with You

Some of the best multi-generational homes aren’t perfect on day one—but they have potential:

- Unfinished basements

- Bonus rooms

- Garages that could later be converted to living space

- Second kitchens or space that allows for one in the future

- Lot space to build a DADU (Detached Accessory Dwelling Unit)

This allows families to start simple and adapt over time, rather than overpaying upfront or moving again later.

Aging in Place Is Cheaper, and Kinder

Small design choices can make a home work for decades:

- Main-level bedroom and bathroom

- Walk-in showers

- Minimal stairs

- Wider doorways and hallways

These features cost far less than assisted living and allow people to remain independent, familiar, and connected to family.

Clear Agreements Protect Relationships

Even when it’s family, clarity matters. I always encourage:

- Simple written agreements

- Clear expectations around costs, timelines, and exits

- Respectful conversations before emotions get involved

Structure doesn’t reduce love; it protects it.

Privacy and Sound Matter More Than You Think

Noise is the number one reason multi-generational living breaks down. Small investments like:

- Solid-core doors

- Extra insulation

- Separate heating zones

can make a huge difference in daily comfort and long-term success.

Care Without “Institutional Living”

Multi-generational homes can provide:

- Daily check-ins without constant supervision

- Space for a future caregiver if needed

- Support without stripping autonomy

This preserves dignity and avoids the emotional and financial toll of institutional care whenever possible.

Always Stress-Test the Numbers

Before buying, it’s important to ask:

- Can one unit cover 30–50% of housing costs?

- If someone moves out, is the home still affordable, or could it be rented to someone else?

- Could the property work as a single-family home regardless?

Flexibility is what keeps a good plan from becoming a burden.

Why This Matters

Assisted living can cost $6,000–$8,000+ per month, often draining savings quickly. Multi-generational house hacking can:

- Keep families together

- Reduce monthly expenses

- Preserve independence

- Build and/or protect wealth

- Provide care with compassion

If you’re thinking about buying your first home, moving up to a larger home from your first home, helping aging parents, need a gentler floorplan, planning for retirement, or simply exploring options, I’m always happy to talk through what’s possible. Housing should build wealth and support life—not limit it. Please reach out if you’d like to discuss viable options for your family’s housing, wealth-building, and sustainability.